Guest Post: "Pension Crisis Averted" by @pdxsag

[This is a guest review by our CBS correspondent @PdxSag.]

Hypothesis: Spike protein gene therapy shots (the mRNA vaccines) might age the cardiovascular system and increase cancer risk by 10 years, or around one Gompertz interval.

Some puzzles that I sought to answer in formulating the hypothesis:

- Mortality worsened in 2021 vs. 2020 despite widespread vaccinations.

- A "spike" (pun!) in mortality among younger, working-age individuals coincided with vaccine mandates.

- The spike in younger deaths peaked in Q3 2021 when Covid deaths were extremely low (but rising into the end of September).

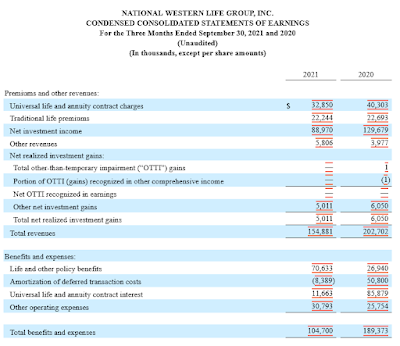

The conundrum is showing up most clearly in life insurers' results. Here, for example, is the NWLI income statement for Q3 2021:

Death benefit pay-outs up by over 2.5X? It’s like these guys were underwriting life insurance in SF in 1985. And now we are seeing that Q4 2021 loss ratios have increased huge percentages over the Q4 2019 figures. Edward Dowd has started documenting life insurance company financial results for the 4th quarter 2021, and they are not good. Working-age claims (presumably the 55-65 demographic) are running 30-60% above pre-vaccine year-ago quarters of 2019 and 2020. Many life insurance companies swung from quarterly profits to losses. [ZH]

My hypothesis, that the spike protein is essentially doubling the mortality rate, may seem extreme. But that is what it would mean if it simply aged everyone by about eight years - again, one Gompertz interval.

Odds of dying in 10yrs [1]:

60 yo's -- 15% -> 30%

70 yo's -- 30% -> 65%

80 yo's -- 65% -> 95%

90 yo's -- 95% -> 99%

Present day, number of Americans [2]:

55-65 yo's 24M

65-75 yo's 18M

75-85 yo's 12M

85+ yo's 4M

Therefore, in 2030 revised demographic counts:

65-75 yo's 21M -> 18M

75-85 yo's 12M -> 6M

85-95 yo's 6M -> 0.6M

95+ yo's de minimis

That is a 66% drop in the right-tail, and twice as many early deaths among the youngest cohort of pensioners. Pension obligations fall commensurately: pension crisis averted. Medicare and post-retirement health obligations are probably reduced as well.

This bears watching closely in the year ahead. Unlike the “trust-science” propaganda, death benefit payouts don't lie and can't be gamed. Finally, increased claims, and if we get them, rising interest rates are not going to be kind to most life insurers.

Life insurer results for Q2-2022 will tell the tale. Q1 confounded by boosters. If Q2 comes in ugly then we’ll know the damage is likely cumulative and long-term.

![]()

1 comment:

Q2 results have come in. What do you think they show regarding your thesis?

Post a Comment