Tobacco Earnings - Q2 2022 ($MO $BTI $PM $SWMAY)

Tobacco stocks had a bit of a rough quarter and have had a rocky year so far. Altria fell from a 52 week high of almost $56 to as low as $41, but has recovered to about $44. Philip Morris collapsed from a 52 week high of almost $110 when Russia invaded Ukraine, almost got back there in late May, but took a tumble as well. British American Tobacco was affected by Russia/Ukraine exposure as well, and had a particularly ugly day this past Friday.

We don't care so much about the share prices, we care about how the businesses are doing and what kind of owner earnings and dividends we will be receiving. Maxim: "share prices are more volatile than corporate cash flow, which is more volatile than asset replacement cost." So, let us take a look at the product sales and earnings for our four companies.

British American Tobacco

British American Tobacco (previously) sells cigarettes (Camel, Lucky Strike, Newport, American Spirit) and "New Categories" (safer nicotine) products: the Vuse vape, the Glo heat not burn product, and Velo "modern oral" nicotine pouches. The safer nicotine products grew revenue 45% for the first half of 2022 vs 2021, and now represent 15% of total revenue. The biggest contributor is the Vuse vape product, responsible for about half of total new category revenue. Also notice that new category revenue was up more than volumes meaning that these products have pricing power. (But note that the reduced risk product category is not making money yet - the new category segment lost about $300 million the first half of 2022.)

In the U.S., the new category revenue was up 70% (1H 22 vs 1H 21), and that is almost entirely from the vape product. (Re-nicotinization! The concept is taking off.) Also noteworthy, the U.S. cigarette volumes were down 13% but revenue was still up 3% (though down 3.4% in constant currency). Overall, profit was up 9% in the U.S. and operating margin here improved slightly to 47%. Here is what management said about its U.S. vaping regulatory progress:

In May 2022, we were delighted to receive Vapour marketing authorisations for Vuse Ciro and Vibe in original flavour from the FDA. Together with our Vuse Solo authorisation from last year, this gives the Group the broadest portfolio of market authorisations provided to any vapour company in the U.S., and we believe it also supports further confidence in our Vuse Alto Premarket Tobacco Product Application (PMTA), which shares the same foundational science. Subject to the ongoing FDA discretion, all Vuse products currently available in the U.S. may continue to be marketed.

BTI had a market cap of $92 billion and net debt of $50 billion dollars for an enterprise value of $142 billion. During the first half of 2022, BTI generated about $5.2 billion of cash flow and returned $4.5 billion to shareholders. If you annualize that, it is a cash flow yield on the enterprise value of about 7%. The earnings multiple on the stock will of course be more attractive than this because of the leverage, probably about 10x or just below.

Altria

Altria (previously), of course, sells Marlboro cigarettes, Copenhagen and Skoal oral tobaccos, the On! nicotine pouch, and owns 35% of Juul, 10% of BUD, and 45% of Cronos.

During the second quarter, Altria's smokeable products segment reported domestic cigarette shipment volume decreased 11.1%. That is a bad decline, but it was during the quarter with sky-high gasoline prices. Also, revenues net of excise taxes were only down 0.7% and the operating income for smokeable products was only down 0.5%. (It was $2.76 billion for the quarter and $5.3 billion year-to-date.) The smokeable operating margin is 59%.

Selling Marlboros in the U.S. is still a business that makes close to $11 billion a year pre-tax. Altria's market capitalization is $79 billion and enterprise value is $108 billion. The market cap of BUD is $92 billion, which is $9.4 billion for Altria's stake. If you adjust for that the MO market cap is $70 billion and the EV is $99 billion. So the valuation for the tobacco/nicotine business is currently about an 11% FCF yield on the EV, and about 8 times earnings. (And that is ignoring whatever value Juul and Cronos may have.) (Their guidance is for 2022 full-year adjusted diluted EPS in a range of $4.79 to $4.93, which would be a 9x P/E on the low end.)

Oral tobacco (which inclides on!) made $430 million in Q2 and $837 million YTD. Altria paid $11.7 billion for U.S. Smokeless Tobacco in 2008 and also got Ste. Michelle Wine Estates, which they sold for $1.2 billion last year. It was a great acquisition.

What is sad is that the failure of the panicked, desperate investment of $13 billion in Juul at a $38 billion valuation has made them shy about strategic investments. I thought that Altria could and would buy Swedish Match:

If Juul's PMTA is approved, it makes sense for Altria to take-under the remaining Juul stake that it doesn't own, possibly structuring the transaction in a way that sheds the startup-era liabilities. (Maybe a bankruptcy or purchase an exclusive license of Juul combined with a sale of their minority stake back to the company for $1 to realize the tax loss.)

Altria should reunite with Philip Morris, and together they should buy Swedish Match. Together they would have the #1 cigarette (Marlboro), #1 closed tank vape (Juul), #1 oral nicotine lozenge (Zyn), #1 snus (General), #1 heat not burn tobacco product (IQOS), and the #1 and #2 dipping ("moist snuff") tobaccos (Copenhagen / Skoal).

And then... no more acquisitions! All that cash flow could roll on home to shareholders.

But as is often the case, after making one type of error (of commission), they proceed to make the inverse type (of omission). They are letting Philip Morris steal Swedish Match, which would've been a great acquisition in its own right, and a blocking move against PM, who want to take away distribution for IQOS from Altria and use the network Swedish Match has built up in the U.S.. Altria isn't even lobbing in a bid to make it more expensive for PM!

Altria's on! product is junk, so their only hope of being involved in re-nicotinization is to get PMTA approval for Juul. (Which is a great product.) The good news is that at the price we are paying for MO, we should do OK even if none of the reduced risk bets work out and we just get the tobacco earnings runoff. It is also interesting that tobacco gets hurt when oil prices squeeze and will presumably benefit in Q3 now that oil has fallen - it diversifies the energy portfolio.

Philip Morris

Philip Morris (previously) reported cigarette volumes up 1% in Q2 versus the prior year and heated tobacco units up 1.9%. (These numbers are dragged down by the loss of Russia and Ukraine business.)

Net revenues for the quarter were flat at $7.8 billion and operating income was down 2% at $3.1 billion. Note that the E.U. region contributes half of PM operating income ($1.55 billion) and the next largest, Middle East & Africa, contributes $500 million.

The current market capitalization at $99 per share is $153 billion, and the enterprise value is $178 billion. During the first half of this year, the company has generated about $4.8 billion of free cash flow. (And has returned $4 billion to shareholders, mostly through dividends.) This is pretty consistent with our past thinking of $10 billion of free cash flow for the year. (Current management guidance is $10.5 billion for this year.)

That puts PM at a FCF/EV yield of 5.6%, noticeably more expensive than BTI or MO. The valuation premium exists because PM has a cigarette business that is still growing volumes, has a strongly growing reduced risk business (revenue up 10% over last year), is more geographically diversified, and in recent years has allocated capital better than Altria. You'll notice that when the regulatory capture revolving door swings, PM is where you go:

A Food and Drug Administration official with considerable power over authorization decisions for e-cigarettes and products aimed at curbing smoking resigned on Tuesday to work for Philip Morris International, the global tobacco conglomerate and maker of Marlboros.

The official, Matt Holman, was chief of the office of science in the agency’s Center for Tobacco Products. In a memo to the staff on Tuesday, Brian King, the center’s director, wrote that Dr. Holman had announced that he would be leaving — effective immediately — to join Philip Morris. The memo said Dr. Holman had been on leave and, consistent with agency ethics policies, had recused himself from all tobacco center work “while exploring career opportunities outside of government.”

An example of the great capital allocation is the purchase of Swedish Match. While I suspect that they are going to have to raise their bid, they're probably going to pay on the order of what Altria paid for just a 35% stake in Juul, and get whole ownership of a business that earns $643 million net, growing at a double digit rate.

Swedish Match

Swedish Match (previously) reported smokefree sales up 29% in the second quarter, with revenue in the US up 26%. We had called Swedish Match our "growth stock," and it looks as though it is going to be stolen from us too soon. (CBS: "Our style of value investing rarely buys hockey stick growth, but here is hockey stick growth available for 18x earnings.")

As most are already aware, Philip Morris reached a deal to acquire Swedish Match for SEK 106 per share. (That is USD $10.47, a market capitalization of $16 billion.) While we think that PM will have to up their bid, it appears likely that this business is going to go into the PM fold, where it will contribute to profits and be used as a battering ram against Altria's on! and as a backdoor to distribute IQOS in the U.S. without Altria. Also disappointing that the Swedish Match board didn't negotiate for PM stock - we would rather be able to roll the exposure into PM tax-free.

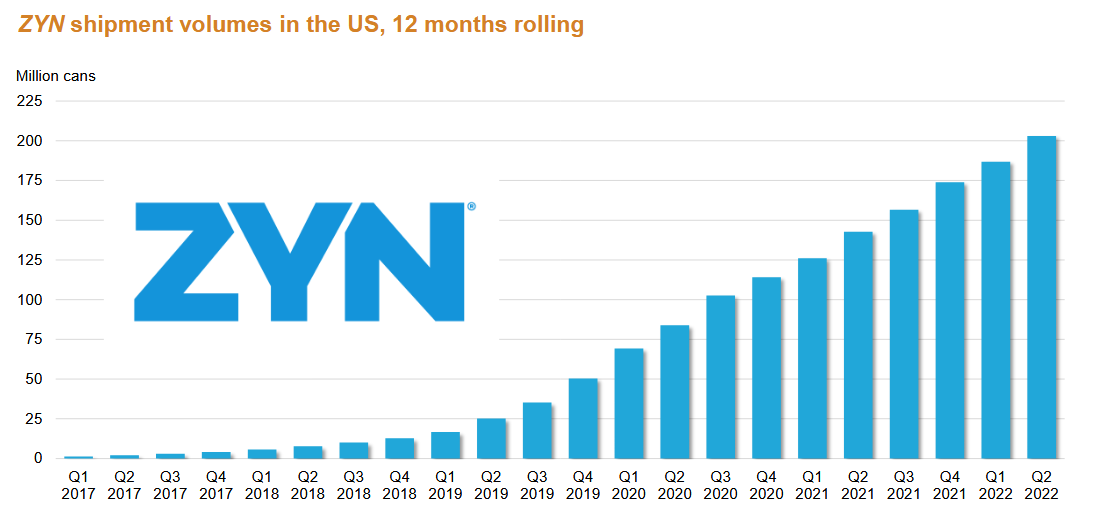

Swedish Match was a great investment but it is also interesting because of what it is saying about re-nicotinization. Given a safe way of dosing nicotine (such as an oral pouch with no tobacco leaf carcinogens), thoughtfully designed with good user attributes, lots of people who were never smokers are going to want to use nicotine for a mood/productivity boost. (See Tucker Carlson and Edward Luttwak.) From the Q2 call:

[T]he nicotine pouch category is rapidly growing relative to cigarette. Measured by volume and according to IRI data, and we make 1 can of nicotine pouches equivalent to 1 type of cigarettes, nicotine pouch volume for the year-to-date period was well above the 10% benchmark in the west and exceeded 4% on a national level. Based on indications of average weekly consumption levels for consumer ranging from 2 to 3 cans, our estimate of the number of ZYN users relative to the number of cigarette smokers on a national level is in the range of 5% to 7%.

The FDA is attempting to stand in the way of beneficial re-nicotinization, just like they are constantly gunning for our OTC supplement regimens. But in a sclerotic country, it may be good to bet on regulatory capture and the status quo prevailing.

![]()

1 comment:

Swedish Match CEO on call:

take nicotine pouches, we did take pricing this year on ZYN. And then from time to time, we have some promotional programs as well, but nowhere near in depth our largest competitors.

Over time, we believe that there are pricing opportunities also in nicotine pouches, but the competitive situation is very intense in this state of the extreme growth in the category.

Meaning, Altria dumping their on! garbage...

Post a Comment