Philip Morris International Inc. ($PM) - Q1 2023 Earnings

PM reported earnings and gave an investor presentation this morning. The current market capitalization (at $97 per share) is $150 billion and the enterprise value is $193 billion. Operating income in Q1 was $2.8 billion at a 34.1% margin. Smoke-free product revenues were 34.9% of total revenue. Total volume shipped was down 1.1% with heated tobacco up 10.4%. Management guidance for this year's adjusted diluted EPS is $6.10 to $6.22 per share, which puts the shares at just shy of 16x earnings. If they hit their guidance for 2023, that would be 7-9% growth in EPS over 2022 earnings.

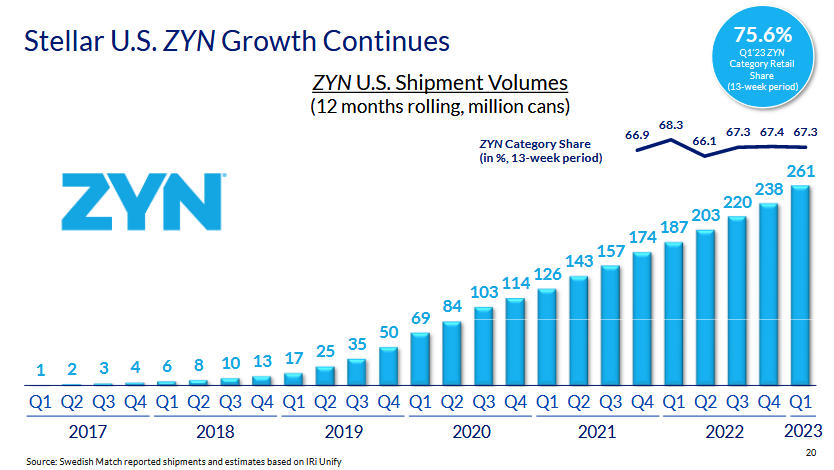

Almost painful to see how well Zyn is doing after the Swedish Match acquisition. If it were still a stand-alone entity, it seems likely that we would have consolidated all of our tobacco investments into it (in order to escape Altria's Bungles and the problem of the vaping competition free-for-all). The Zyn market share is 67% and the value share is 76% - this is a stronger monopoly than any cigarette brand or company has ever achieved.

Highlights from the conference call:

- I am pleased to report that Q1 performance exceeded our expectations, with strong underlying momentum from IQOS, ZYN and our combustible business. As mentioned at our full-year earnings in February, we expected this quarter to be the weakest of the year due to a confluence of transitory factors impacting our top- and bottom-line. In this context, our business delivered robust results and we look forward with confidence to the remainder of the year.

- Smoke-free net revenues made up almost 35% of total PMI, despite the impact of adverse timing factors on HTU shipments, with an increasing number of markets crossing the 50% threshold.

- In combustibles, accelerated pricing across a range of markets helped to deliver robust organic net revenue growth. Swedish Match delivered impressive results, with a stand-out performance from ZYN’s 47% U.S. shipment volume growth compared to the first quarter of 2022.

- While the increasing mix of HTUs in our business, at higher net revenue per unit, continues to positively impact our performance, lower shipments in Europe this quarter due to wholesaler and distributor inventory movements limited the benefit.

- Our updated full year adjusted diluted EPS forecast of $6.10 to $6.22 includes an estimated unfavorable currency impact of 30 cents. Positive estimated impacts from the Euro and a number of other currencies are outweighed mainly by the weakness of the Japanese Yen, as well as the significant depreciation of the Russian Ruble and the Egyptian Pound.

- Let’s examine ZYN’s recent U.S. performance in more detail. Superb progress continues with a record increase in 12-month rolling shipment volumes of 23 million cans, which equates to 40% growth. Category volume share remained essentially stable despite continued heavy competitive discounting from less premium offerings. Importantly, retail value share for ZYN also remains strong at 75.6%, highlighting its premium positioning and superior brand equity. There are two key engines driving the U.S. growth of ZYN, as covered at CAGNY. First is the progressive increase in distribution, with the number of stores 13% higher than Q1, 2022 at around 140,000. There remains ample opportunity to further increase this over time. Second are velocities, or the number of cans sold per store per week. ZYN velocities continue to grow sequentially and by an impressive 21% compared to prior year as the brand continues to resonate with adult nicotine users.

- We continue to work on our IQOS U.S. commercialization plans for launch in Q2 2024, in line with the principles outlined at the recent CAGNY conference. With the benefit of the expertise and commercial tools from launching IQOS successfully in over 70 international markets, and a U.S. market with a clear regulatory framework and the ability to communicate with adult smokers, we remain very positive about the opportunity. Importantly, we believe we can make the necessary investments in the U.S. business, generating additional top-line performance while continuing to deliver strong bottom-line growth for PMI during the investment period.

- Another key mid-term opportunity from the Swedish Match combination is the international expansion of nicotine pouches, notably with ZYN -- the world’s leading brand.

- While staying clearly focused on the heat-not-burn and nicotine pouch categories, which present the largest and most accretive growth opportunities, we are adjusting our VEEV e-vapor portfolio and approach. We intend to focus on commercializing in select markets and prioritizing profitability given the known category challenges. VEEV ONE is a new pod-based system providing an enhanced user experience with fully outsourced manufacturing of devices and consumables to optimize costs. VEEV ONE will replace the current VEEV product and, as a result, we no longer intend to file a PMTA for the former technology. Instead, we will focus our near-term FDA engagements on IQOS and ZYN. We will come back on future e-vapor FDA authorizations in due course.

- I think we've already been clear that while we were clearly developing some offering on the vaping category, this was not our priority. We had IQOS. And now I would say we are even more taken by two priorities, which are IQOS and ZYN. When you have such a fantastic team and the potential that they have to deliver very strong top line growth, volume growth, revenue growth and in a very nicely profitable fashion, that's really the priority. I guess you listened to us at CAGNY and we expressed the questioning that we have on the vaping category today, which are around the absence of clear regulation in many country. The fact that, that is giving way to an appropriate marketing activities, risk of underage consumption. And also the fact that this is a category where so far it's difficult. I'm not saying impossible, but difficult to see a lot of profitable model being developed.

An interesting discussion in the Q&A about how European cigarettes are holding up better than U.S.:

- [Gaurav Jain] [T]he U.S. cigarette volumes industry level are quite weak, minus 9%. And then looking at the European data that you shared, it is -- the industry volumes are flat on what were already very strong comps. And the reasons what have been mentioned for the U.S. industry weakness, which is macro, weak consumer, stimulus payments going off, disposable e-cigarette growth, I could apply the same logic to EU consumer -- EU smoker and still the volumes are so much better than trend. So is there a -- can you explain like why are the U.S. smoker and EU smoker, why are they behaving so differently?

- [Emmanuel Babeau] Gaurav, I cannot -- and I will have to consider that I'm not the greatest specialist of the U.S. consumer for combustible cigarettes. So I wonder myself to given an analysis. I think it's in line with my previous comment on the fact that so far, we have been a pretty good resistance from the consumer to same price increase and coping with inflation in Europe. I'm not able to tell you why there is a difference here. We know that the social model in Europe is different. You may have some more protection, some more safety needs that are playing and maybe limiting the impact of inflation. There was maybe more compensation given from various government on trying to fight again energy price increase and sometimes compensating of agricultural product inflation across a number of geographies. So that can be one element to explain why the European consumer is resisting better. But I'm not going to pretend that I have the perfect answer to your question.

Still hoping that PM can get a hold of Juul cheaply and get it FDA-authorized in the U.S. The comment about the challenges of vaping are not so encouraging on that front, but at the same time PM are clever negotiators and play their cards close to their vest. This could be a way of softening up the Juul shareholders. And at least we know that PM is not likely to blow $3 billion on an unprofitable vape company.

![]()

2 comments:

Earnings yield on PM: 6.25%

Dividend yield on PM: 5.14%

Yield on PM 2043 maturity (20 year): 5.6%

"Earnings yield on PM: 6.25%

Dividend yield on PM: 5.14%

Yield on PM 2043 maturity (20 year): 5.6%"

Point is they shouldn't need much capital at all to grow a whole lot. Volumes relatively stable, prices up mid single digits, IQOS and Zyn taking share in the US, etc. Equity pencils out to low to mid teens. Give me that over the bonds all day.

Post a Comment