Cheap Cyclicals and Value vs Growth

The market capitalization of United States Steel Corp (X) is only $7 billion. That's about equal to its tangible book value (see latest 10-Q), which is pretty impressive since it was incorporated by J.P. Morgan in 1901.

I think they are something like 10% of U.S. steel production market share. For the first nine months of 2021, they had $14.7 billion of revenue and $3.1 billion of reported net income. Their capex is actually less than depreciation so free cash flow is meaningful as well. They're using it to pay off debt, pay a larger dividend, and buy back stock.

Shares are trading where they were in 2004-2005. That is a pattern common to all of our "cyclical" company investments. The Dorchester Minerals partnership units trade where they did 15 years ago too. So do Suncor shares, British American Tobacco, Pardee Resources, and many other "hard asset" and "resource" type companies. The energy sector ETF (XLE) has been flat (with big swings, of course) for fifteen years.

During the same period of time, the NASDAQ 100 has gone up about tenfold. Over the past 15 years, you couldn't go wrong buying a "compounder," couldn't go right buying a "cyclical".

So now you can buy a steelmaker for 1x tangible book value (historical cost less depreciation) and under 2x earnings. Meanwhile, $7 billion would barely buy you anything in the Ponzi growth part of the market.

- Beyond Meat has a $4 billion market cap.

- The EV scam company Nikola still has a $4 billion market cap - with no revenue.

- The 30th largest cryptocurrency by market capitalization ("Fantom") is the same market cap as U.S. Steel.

A fellow on Twitter has put together something called the "Double Dog Index": it is a basket of companies that are projected to "earn the majority of [their] mkt cap in FCF in next 4-6 quarters," have "a relatively clean capital structure (i.e., not over-levered or w/ debtholder vs stockholder conflicts)," have "reasonable management (i.e., not a stock that 'nobody will touch' due to past mgt transgressions)," are "not publicly opposed to capital return," and are not "special situations".

His list has coal companies (including ones with significant revenue from metallurgical coal for steelmaking), U.S. Steel and Canadian Steel maker Stelco Holdings, Chilean copper producer Amerigo Resources, nitrogen fertilizer producer CVR Partners, pulp and paper manufacturer Resolute Forest Products, Israeli shipping company ZIM, lumber company GreenFirst Forest Products, and nitrogen fertilizer company LSB Industries.

It is particularly interesting to see this undervaluation of cyclicals in industries besides coal or oil. That means it is not just the "energy transition" or fossil fuel divestment responsible for the low multiples. In fact, those themes, if they in fact played out, ought to be bullish for steel demand in particular. Here is how the Double Dog author describes the disconnect:

You need to understand that the $ARCH investment setup is available across a wide range of commodity sectors at the moment. Don’t waste your time trying to understand ‘what’s wrong’ or that ‘somebody knows something’ about ARCH. Frankly, a lot of talented commodity equity folks have been blown out in the last decade. We have just come out of a fallow period and there is max macro uncertainty. On top of this, you are messing with the oldest cyclical maxim in the book - you want to pay a high multiple when things look dire, not a low multiple on blowout earnings. There is so much pattern recognition out there that this is how you trade these stocks - and this is another reason why you are seeing this opportunity on your screen.

Yes, macro could be abysmal from here. Yes, there is evergreen idiosyncratic risk in all of these names. But if you truly believe you are generating this amount of cash on a debt free company with somewhat competent management, you just have to bet. What you’re not even considering is that the duration of these high prices could last longer - who knows what could cause the next bottleneck. You are also buying in Year 1 of a bull market after a vicious bear market that restrained investment in many different commodity subsectors. The ‘never pay a low multiple maxim’ was usually a good rubric when we were many years into an upturn. And by the way, Buck, I actually think we might have a real economic recovery in the next 3-5 years, not that pathetic post Financial Crisis drivel that we all struggled through!

What is happening with cheap cyclicals is a perfect example of a redemption flywheel, as described by Lyall Taylor in his two important essays, Market inefficiency, liquidity flywheels and Unravelling value's decade-long underperformance (and imminent resurgence). As I wrote last March,

Lyall’s liquidity and redemption flywheel theory would mean that instead of a bubble making it so that you have to sit on your hands, a bubble causes the tide to go out from investments that are “cold” and we should be looking for those. Based on the theory, they would be investments that had done poorly recently for whatever (possibly idiosyncratic) reasons of their own and suffered a positive feedback loop of selling. His theory implies that the very end of a secular trend in growth vs value would be a crescendo of selling in some areas (that creates the "value") and buying in the other areas (momentum ones, which become very overvalued). And then after the crescendo, the trend would reverse sharply.

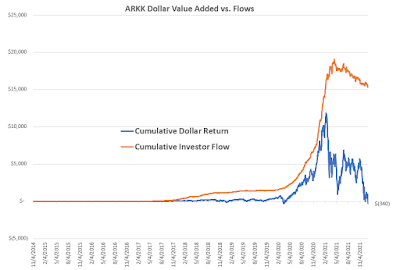

If Lyall's model is correct, it is clear where the value isn't - the stuff that went parabolic at the same time it had big inflows of capital:

And it's also clear where the value is, or should be. The stuff that has been in a bear market for fifteen years; the cyclicals:

I want to wrap this up by emphasizing that, while I used X as an example, X is by no means unique in the commodity space. Near across the board, I’m seeing commodity companies that have been minting cash flow for the past ~6 months but are trading at insanely low valuations / haven’t seen their stocks budge despite the record cash flow. [...]There is so much cheap stuff it's hard to pick. We are already full on hydrocarbons (royalties and Canadian oil), pipelines, tobacco, and small financials. But with incremental capital (dividends and new inflows) it seems compelling to diversify into other cheap cyclicals.

All I’m trying to point out is that these stocks have not budged after six months of producing record results, and the cash flow to remaining enterprise value dynamics are getting pretty wonky. Each has idiosyncratic risks, but it sure seems like a basket of them will do well absent an [imminent] and deep recession.

![]()

13 comments:

On U.S. Steel, CapEx is about to step up substantially because they're building another EAF. See slides 13-16 here: https://s26.q4cdn.com/153509673/files/doc_financials/2021/q3/U.-S.-Steel-3Q-2021-Earnings-Presentation1.pdf) The return on that CapEx is unclear (at least to me).

The general point, though, remains: current equity prices of commodity producers appear to imply an imminent sharp declines in commodity prices. Maybe that happens, and maybe it doesn't.

I'm skeptical, though, of any thesis that relies on management devoting nearly all cash from a 2021-22 windfall to share buybacks. The creator of the Double Dog Index, for example, models that for Arch Coal. But Arch Coal management seems much more interested in paying off debt and building cash reserves, perhaps because they're worried that ESG is going to freeze them out of capital markets.

I also looked quickly at Amerigo. In light of its royalty obligations, what copper prices does it actually need to be a good investment?

Thanks for comment.

I think the general point is a bit broader that what you stated.

For oil and gas and coal companies, perhaps it's the "energy transition".

For "commodity producers," perhaps it is "imminent sharp declines in commodity prices," as you say.

But what about pipelines? A diversified basket trading at a 17% discount to NAV with a 7% distribution yield:

https://cef.tortoiseecofin.com/funds/ntg/

Individual names trading at 10x distributable cash flow:

https://finance.yahoo.com/quote/MMP?p=MMP&.tsrc=fin-srch

https://www.creditbubblestocks.com/2021/03/magellan-midstream-partners-lp-mmp.html

Small banks with 10% ROE (1% ROA) are trading for less than tangible book... like 85%. Worth more dead than alive.

Did you read those two Lyall Taylor essays? I think the redemption flywheel theory explains it best.

I agree with Taylor's general points, particularly the massive reflexity (higher prices creates demand, rather than restrain it) that comes from third-party management of assets and indexing.

I was more noting the big difference in business quality between the companies in the Double Dog Index and, for example, Williams, Enterprise Products Partners, and Magellan in pipelines, or Altria and BAT in tobacco. You can put something like Lockheed in that category too, though it has less of an ESG taint.

Following on the from the quality discussion, with the companies in the Double Dog Index, you need to keep your wits about you and have an exit plan, because I doubt you want to be a long term investor in, for example, steel production and shipping. Williams, EPD, Altria, and BAT don't present the same issue.

Apropos of my prior comment on relative quality, see: https://finance.yahoo.com/news/stelco-q4-2021-shipments-lower-123000147.html

If an Altria production facility had an issue that pushed some shipments a quarter or two, what difference would it really make? Compare that to a thesis that depends on once-in-20 year windfall profits over the next few quarters. Of course, that's one of the reasons to buy a basket of these deep cyclicals rather than try to pick one.

Maybe we have the right answer already, then, with the particular hydrocarbon, pipeline, tobacco, and royalty investments that we already thought of?

It all started with this thought experiment:

https://www.creditbubblestocks.com/2020/10/what-i-would-buy-instead-of-tesla.html

We put special thought into finding companies where we could be long term (hopefully permanent) investors. The reason for that is that we would prefer not to have to sell and pay tax on nominal gains from inflation.

A big concern was avoiding reinvestment risk and empire building:

https://www.creditbubblestocks.com/2015/02/capital-allocation-problem-in-oil-and.html

I owned X in early 2005 when the situation was similar: demand suddenly grew after years of overcapacity and low prices, customers weren't prepared and reacted to shortages by double-ordering, etc. When the double-ordering slackened, the company went from record earnings to reporting a small loss in six months. And that was while end-user demand was still growing strongly.

Good post, great blog.

I like Ternium (TX) better than US Steel, but that's just me.

"2021 was a year of records and we delivered with record earnings and free cash flow and record safety, environmental, quality, and reliability performance," commented U. S. Steel President and CEO David B. Burritt. "We enter 2022 from a position of strength and are relentlessly focused on continuing our disciplined approach to creating stockholder value. Our balance sheet has been transformed, record cash significantly de-risks strategy execution, and our capital allocation priorities have enhanced direct stockholder returns. We are a fundamentally different company from a year ago and expect 2022 to be another strong year."

https://finance.yahoo.com/news/united-states-steel-corporation-reports-211700625.html

When Cleveland-Cliffs acquired AK Steel in March of 2020, AK Steel, as a stand-alone company, was ready to walk away from electrical steel. It was ready to shut down Butler Works in Pennsylvania. Butler Works produces electrical steel, a type of steel used to make transformers. If AK Steel had done that as a stand-alone company, today the U.S. would not be able to produce any grain-oriented electrical steel for transformers or nonoriented electrical steel, among several other things. That was the scenario that I inherited at Cleveland-Cliffs, as far as electrical steel goes, when we acquired AK Steel. Then, I made the decision not to shut down Butler Works, and now Cleveland-Cliffs is the only producer of grain-oriented steel products in the U.S.

https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/us-electrical-steel-output-vital-to-infrastructure-plans-8211-cleveland-cliffs-ceo-67766869

Huge U.S. Steel profits in Q2...

“Our record-best second quarter was driven by strong performance across our diverse operating segments,” commented U. S. Steel President and Chief Executive Officer David B. Burritt. “As we continue to demonstrate the execution of our strategy, it is timely to reflect upon just how much progress we’ve made over the past twelve months, exhibiting continued record safety performance, generating nearly $6.7 billion of adjusted EBITDA and over $4 billion of free cash flow, building over $3 billion of cash, and returning nearly $850 million to stockholders, including July's buyback activity.”

https://investors.ussteel.com/news/news-details/2022/United-States-Steel-Corporation-Reports-Record-Second-Quarter-2022-Results/default.aspx

The average realized price of flat rolled and mini mill steels for U.S. Steel YTD was about $1,350/ton.

The current price is under $800/ton:

https://quotes.ino.com/charting/?s=NYMEX_HRC.Q22

That level is more like the 1H of 2021 when the average realized price for U.S. Steel's flat-rolled was under $1,000.

Segment earnings for 1H 2021 were only $725 million as opposed to $1.3 billion the first half of this year.

So, be prepared for Q3 2022 earnings to be lower than recent quarters.

(See HRC steel historical price chart: https://tradingeconomics.com/commodity/hrc-steel)

Historically (over the past decade) U.S. Steel has not been all that profitable: https://www.macrotrends.net/stocks/charts/X/united-states-steel/operating-income

The market price of X basically implies that this spike in steel prices and company profits will be short lived.

But the question is, how can that be true if we are going to have an energy transition?

https://www.creditbubblestocks.com/2022/01/the-hard-math-of-minerals-why-energy.html

HRC steel had a nice spring bounce.

https://tradingeconomics.com/commodity/hrc-steel

It's hanging in there at $950/t.

Market cap $4.8 billion, EV about $5.8 billion, Q1 EBITDA 427 million, capex $740 million.

Book value $10.3 billion.

It's been a while! Let's look at the Double Dog Index (not including dividends for any of these...):

ARCH +40%

AMR +3.3x!

X +27%

STLC flat

ARG flat

UAN -7%

RFP taken over +35%, also CVR

WHC +2.5x!

ZIM down 80%

GFP down 40%

LXU down 13%

CEIX +3.7x

So the coal did extremely well.

If you had bought an equal basket, it looks like you would be up 50% not even counting dividends.

Post a Comment