Altria Shares Crushed After Cigarette Volumes Drop 11.6% ($MO)

Altria released third quarter 2023 earnings today. Their cigarette revenue was down 5.3% year-over-year and their cigarette operating income was down 1.7%. Their cigarette volumes were down 11.6% year-over-year with Marlboro down 10.5% (so they must have raised prices by 7.1%). Altria CEO Billy Gifford is blaming illicit e-vapor products.

The shares were down more than 8% today. At CBS we had been writing about the illicit vapor threat recently. In May of this year we considered Altria as a short idea:

Another idea for this basket comes from a very important

investing precept: if you sell an investment, you should consider

shorting it. (Since people have a tendency to sell winners too early, a

corollary would be not to sell something unless the valuation is so

extreme that you would short it.) Recall that we sold Altria

last quarter after owning it happily and collecting dividends for

several years. (Dividends are great; you just have to be very careful

that they are sustainable. Altria is a retail investor favorite because of the dividend.)

We sold Altria even though nicotine usage is growing, because the growth is occurring in reduced risk vaping products that are illicit (non-FDA-authorized) yet better than what big tobacco can sell. They are truly being disrupted: these new products are cannibalizing their cigarette sales and impairing the time honored strategy of raising the price of the pack to offset the volume declines.

As of the first quarter, Altria's cigarette operating income was shrinking at a 2.2% annual pace. If you have a ten percent cost of capital, you can only pay 8x earnings for an income stream shrinking at that rate. But the 2.2% that we have just seen is rather trivial. Altria's cigarette volumes actually shrank 11.4% and revenues declined 3.3%, indicating that the price of the pack was increased by a little over 9%.

The question

is, what would happen if that formula breaks? The answer is that

earnings shrink, and the multiple that people will pay for Altria stock

rerates much lower. Let's say that investors have a 10% cost of capital

and they believe that Altria earnings are going into a permanent four

percent annual decline. This could mean ongoing 8% volume declines

coupled with the ability to raise prices only as fast as inflation: 4%.

That would justify a 7x valuation for the tobacco earnings.

That

would justify about $62 billion enterprise valuation on the after-tax

earnings. The current market capitalization is $82 billion, and there is

also about $15 billion of debt net of cash and the (current) value of

the BUD stake. Deduct that $15 billion from the $62 billion pro-forma

value and you get $47 billion for the equity; about 57% of the current

market cap, or a share price of $26. A January 2025 $25 call option seems to be going for $22.4, for a breakeven of $47.4 (versus the

current price of $46.67)

In April we wrote:

Ask yourself why the macro environment is so bad for cigarette sales, yet McDonald's had a great quarter (U.S. comp sales up 13%), Chipotle had a great quarter (comp sales up 11% with margins also up), PepsiCo had a great quarter, and Valero had a great quarter (with demand for gasoline and diesel at record highs).

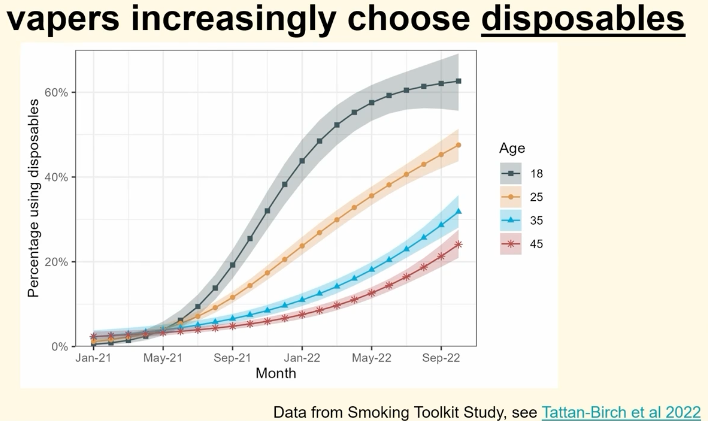

The difference is that cigarettes have better, cheaper competition. There are the "open tank" vapes which the user refills with his own nicotine-containing liquids ("juice"), which we think appeal to the downscale ex-smokers, as well as the pothead users who have experience using them with THC liquids.

For the younger crowd (which probably has never-smokers), you have closed tank products like Juul or the Elf Bar, which are illicit but selling like hotcakes.

The biggest thing that tobacco longs are missing is that competitive intensity in nicotine delivery has gone from sleepy (the cozy Marlboro and Camel duopoly) to ferocious.

That is going to make it very difficult for big tobacco to keep raising the price of the pack of cigarettes enough to offset the volume declines. It is also likely to shrink the overall nicotine delivery profit pool (which is more of a function of industry structure than market size) and divide whatever profit pool does exist among more players.

Bearish. We think the time to get out of this industry is when you see the competitive intensity increasing. By the time it is obvious in the quarterly numbers, it may be too late to sell at a good price.

In March we wrote:

It is seeming possible that re-nicotinization is

happening, but that the nicotine as a service business is going to

remain fragmented enough such that the profit pool that used to exist in

cigarettes is substantially diminished.

Big tobacco is at a disadvantage in vaping because it has been playing by the rules. If you can only sell tobacco flavored vapes, you are going to lose out to "disruptors" who do not follow the rules and can sell watermelon or cotton candy flavored ones. BTI's U.S. subsidiary has asked the FDA to crack down on the illegal vapes, but they are still for sale. Can the FDA stop strip mall vape stores and gas stations from selling Chinese vaping trinkets to willing buyers? It's an open question. They do not have a police force.

And even if they can, what assurance do we have that the authorized reduced risk nicotine market is going to be a profitable duopoly the way that cigarettes were?

And a few days earlier in March:

Right before the weekend, Altria announced

that they sold (really, gave away) their entire 35% stake in Juul Labs,

Inc., for which they paid $12.8 billion, in exchange for "a

non-exclusive, irrevocable global license to certain of JUUL’s heated

tobacco intellectual property". Then today, Altria confirmed

a rumored purchase of NJOY Holdings: they are paying $2.75 billion

(plus a possible further $500 million) for the company, which has an FDA-authorized pod vape called the NJOY ACE.

These are just very discouraging developments at Altria and some tobacco investors are kidding themselves thinking anything else.

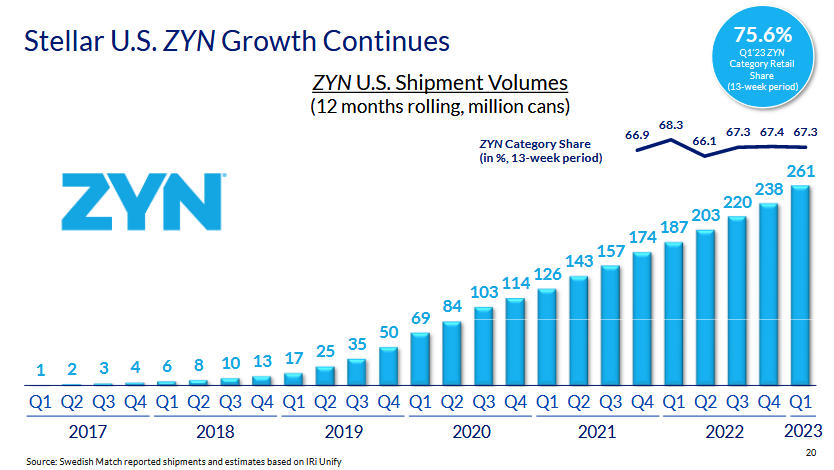

Juul is

the best vaping product, hands-down, the same way that Zyn is the best

oral nicotine product. Last year, Altria let Philip Morris buy -

practically steal - Swedish Match and Zyn without lobbing a bid or even

expressing interest that might have raised the cost for its competitor.

It would not surprise us if Philip Morris gets a hold of Juul (which

still the vape leader with close to 40% market share) and turns it into a

cash cow. (What would be really amazing is if PM uses its regulatory

connections to get an authorization - MGO - for Juul vapes but only

after buying it at a great price.)

But Altria won't make a

penny off of a Juul acquisition or turnaround. All they are getting is a

non-exclusive IP license for heated tobacco, which implies that they

are going to waste more money trying to buy or acquire a heated tobacco

product for the U.S. Didn't they learn from the poor performance of IQOS

in the United States that heated tobacco does not appeal to U.S.

nicotine consumers?